In January, Kline & Company, a worldwide consulting and research firm serving needs of organizations in the lubricants and base stocks industry, introduced its monthly Base Stock Margin Index, a characterization of recent cash margin contributions in the U.S. base oil market over the past 24 months.

The Index estimates cash margin contributions associated with U.S. Group II base stock production. It simulates EBITDA before the deduction of corporate SG&A expenses for typical VGO-based virgin base stock plants and RFO-based re-refineries. A more detailed description of the Margin Index can be found in the January release.

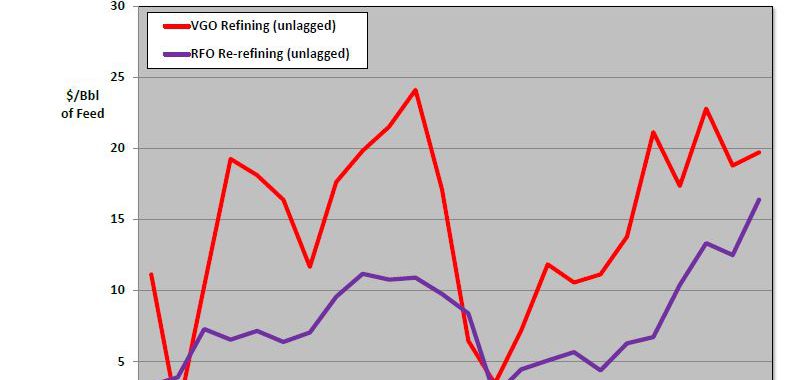

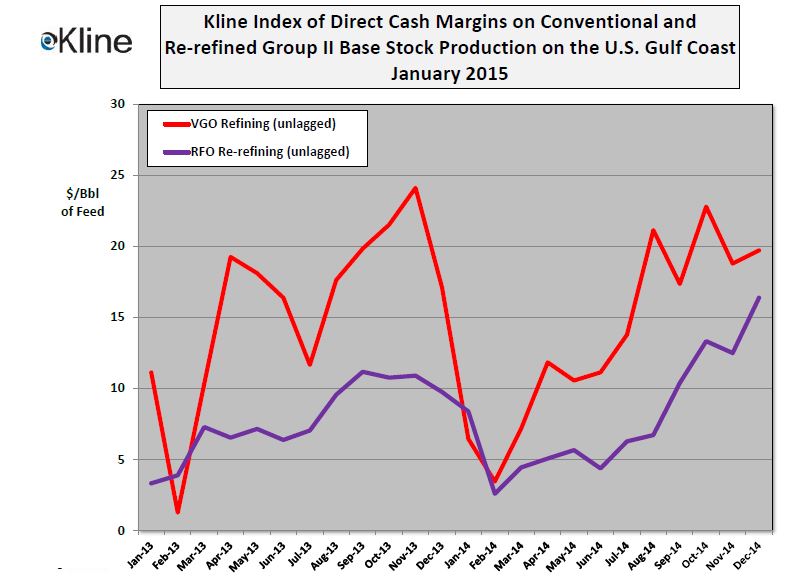

“As the year 2014 ended, the dramatic collapse experienced in oil markets during the fall continued unabated. Spot Brent crude, which peaked at $117/Bbl in early September, fell to $45/Bbl by mid-January 2015. At this price level the bottom of the market seems to have been established. The dramatic decline in crude oil prices has generally been mirrored in commodity fuels markets, though ULSD has regained a premium of some $10-15/Bbl over low sulfur VGO, which had been lost in early 2014. However, base oil markets, already roiled by growing overcapacity and static demand, have followed a somewhat different path,” noted Ian Moncrieff, Vice President in Kline’s Energy Practice. “In a rapidly declining price environment, commodities are most immediately responsive to changes in market fundamentals, while more differentiated specialties, such as base oils, react more slowly. In part, this effect is caused by the physical transformation of feedstocks through the various base stock processing and storage steps, and also the less instantaneous nature of specialty product pricing. This behavior is particularly true in the United States where the majority of contract business is done against variably-discounted posted prices. In Kline’s Margin Index model, we compare contemporary prices of feedstock and products of base oil refining (and re-refining). This comparison produces instantaneous cash margins, as reflected in the above figure. What is noticeable about this chart is the progressive increase in instantaneous cash margins during the past four months as oil prices have dropped dramatically. Is this due to fundamentally improved profitability in the base oil production business in recent months? We think not.”

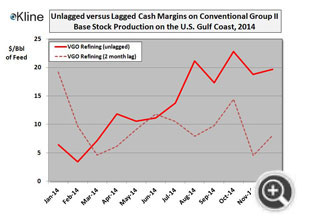

Given that base oil prices typically track feedstock price changes with a two-month lag, Kline has simulated the Margin Index if cash margins are determined with base oil prices against feedstock and other product prices from two months earlier. This lagged calculation, in effect, provides a LIFO accounting view of profit margins (see the chart below comparing lagged and unlagged cash margins on virgin Group II production).

“The accounting (lagged) view of cash margins show a weakening in cash margins which has widened as crude oil prices have continued to fall. Base oil producers have responded more slowly to the continued erosion in oil prices, in the hope that this arbitrage can offset generally weak operating conditions, if only temporarily. Given the expectation of another round of downward adjustments to paraffinic base oil postings in the near future, allied with a stabilization or even modest recovery in commodity pricing, the outlook for instantaneous base oil cash margins is downward.”

For more information on the Kline Index, or to inquire about our pricing and margin analysis services to the base stocks industry, please contact Ian Moncrieff, Vice President (Ian.Moncrieff@klinegroup.com) at (973)-615-3680 in Kline’s Energy Consulting Practice.

For more information on the Kline Index, or to inquire about our pricing and margin analysis services to the base stocks industry, please contact Ian Moncrieff, Vice President (Ian.Moncrieff@klinegroup.com) at (973)-615-3680 in Kline’s Energy Consulting Practice.