This time last year, we explored some of the key consumer trends in the Food, Beverage, and Nutrition industry and considered their impact on ingredients. Now we have a new trend to add to that mix: Global Trade Policy Shifts, and it’s having a noticeable impact on several of these trends and on ingredients themselves.

While the political framing emphasizes trade fairness, the operational reality is far more complex, particularly for food companies managing large-scale procurement and international sourcing networks. We predict a reconfiguration of trade flows and cost structures across several essential food ingredient categories. The implications extend far beyond headline-grabbing tariffs. For food and beverage companies, these shifts demand a recalibration of sourcing strategies, pricing models, and supply risk frameworks, not in six months, but immediately.

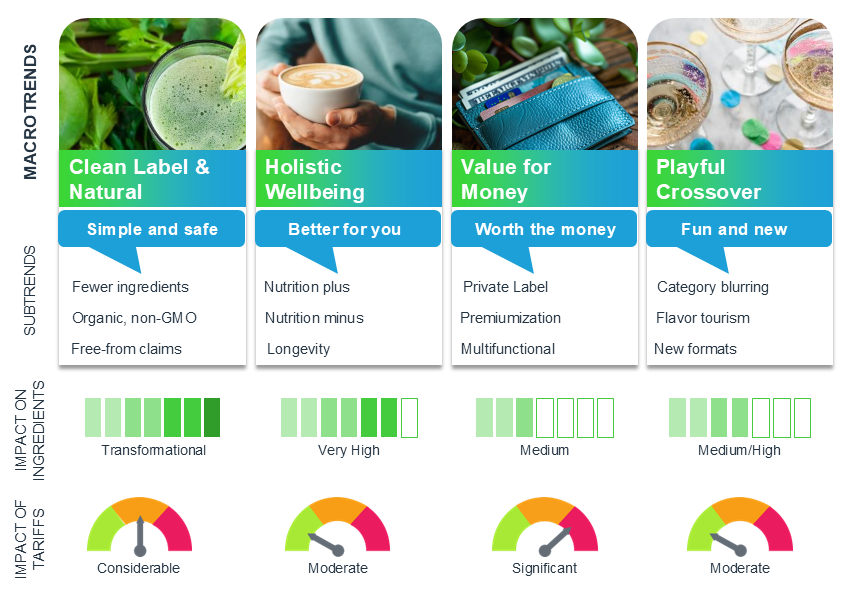

Clean Label & Natural

A key trend overlapping both Clean Label & Natural and Holistic Wellbeing is sugar reduction, and whilst we still expect to see a drive to reduce sugar consumption from food and beverage products, new tariffs could play a role in the sweetener decision-making process when it comes to product reformulation.

Stevia: Under Tariff Pressure, and Under the Microscope

Stevia, the major natural high-intensity sweetener, will fall under tariff pressure as, while some cultivation happens in the U.S., most stevia extracts (like Reb A and the increasingly preferred Reb M) are processed in China and India. With tariffs now reaching 10-15%, cost structures are under pressure, especially for beverage and bar brands banking on zero-calorie positioning. Reformulating around stevia, or reducing its content, can subtly alter flavor perception and mouthfeel, especially in carbonated beverages where formulations have been carefully optimized to balance stevia’s lingering aftertaste.

Monk Fruit: A Niche Sweetener Facing Outsized Tariff Risk

Another natural sweetener facing tariff impacts is monk fruit, a highly prized zero-calorie sweetener derived almost exclusively from China. Used in “sugar-free” or “no added sugar” products, monk fruit offers a clean taste profile and a strong halo of health appeal. Tariffs up to 25% make it significantly more expensive, prompting many manufacturers to either reduce its use or switch to stevia, erythritol, or less natural alternatives. Such changes are not without consequences: consumers accustomed to monk fruit’s clean flavor may notice the shift, and reformulation opens brands to scrutiny over their natural sweetener claims.

Sucralose Gains Strategic Edge Amid New Tariffs

Sucralose, along with acesulfame-K, has been exempted from the new US tariffs, presumably due to its classification under pharmaceutical or food additive categories with strategic relevance. This exemption sharply contrasts with the treatment of other sweeteners like aspartame and polyhydric alcohols (e.g., xylitol), which will be subject to full ad valorem duties. This development may shift sourcing strategies in the sweetener industry, favoring sucralose in reformulation efforts to avoid added tariff burdens. Manufacturers may look to increase imports of sucralose from countries that otherwise would have faced high duties, potentially creating price imbalances in the sweetener market and supply pressures in the short term.

Holistic Wellbeing

Given the exemptions of some key ingredients in this category, the “Nutrition Plus” part of this trend is likely to be less impacted by global tariff reforms.

Vitamins: strategic security and humanitarian supplies

Vitamins produced in China have been exempted from the new US tariffs. The exemption stems from their classification under “strategic security and humanitarian supplies,” alongside pharmaceuticals such as vaccines, biological products, and antibiotics. This includes key vitamin categories widely used in food, feed, and supplement manufacturing such as vitamins A, D, E, K, C, B-complex, biotin, and folic acid. The exemption may help stabilize costs in health-related sectors in the short term, particularly for US buyers heavily reliant on Chinese-origin vitamin inputs.

Value for Money

Several key commodity prices, many of which are already subject to rising prices due to rising production costs and adverse weather events, are set to increase further.

Tea: A High-Value Category with Structural Import Exposure

Tea is one of the most exposed categories under the new U.S. tariff structure. With Sri Lanka now facing a 44% tariff, India 26%, and China 34%, three of the U.S.’s key suppliers are now significantly disadvantaged. There is no domestic alternative. The U.S. does not grow tea at commercial scale. From a supply chain standpoint, this creates both a cost shock and a sourcing bottleneck. For clients with legacy contracts in Ceylon black tea or premium Darjeeling blends, this means immediate revaluation of landed cost and downstream margin. Mid-sized brands will feel it most acutely, particularly those in the specialty and direct-to-consumer segments.

Coffee: The Non-Negotiable Brew

Coffee is a cornerstone of the American beverage market, from hot drinks to cold brews and even protein supplements with mocha notes. With the U.S. importing virtually 100% of its coffee, primarily from Brazil, Colombia, Vietnam, and Ethiopia, a new 10% tariff on green beans represents a direct cost increase for roasters and manufacturers, compounding the already rising coffee price. The ramifications vary by segment. Specialty coffee brands, which pride themselves on single-origin beans and artisanal sourcing, face pressure to either raise prices or sacrifice quality. Meanwhile, large-scale players in the ready-to-drink and private label space may look to reformulate with cheaper blends, running the risk of flavor inconsistencies and consumer attrition. There is no domestic production safety net, making this a raw material price shock with no immediate substitute.

Cocoa: A Dual Shock to Chocolate Supply Chains

Cocoa, the lifeblood of chocolate and myriad dessert products, is under tariff pressure just as global cocoa prices hit decade highs due to weather disruptions in West Africa. With countries like Ivory Coast and Ghana dominating supply, chocolate manufacturers are now squeezed on both ends: raw material costs are climbing due to climate and labor pressures, and U.S. tariffs add a new layer of margin compression. This is particularly problematic for large-volume categories like baked goods, snack bars, and dairy-based desserts, where cocoa is both a flavor and color agent. Reformulating with less cocoa, or replacing it with synthetic cocoa flavors, risks undermining clean-label positioning and product authenticity.

Playful Crossover

With “Flavor Tourism” playing a key role in this trend, several products and ingredients related to this trend will be faced with higher costs as a result of tariff changes.

Tapioca Starch and Bubble Tea Ingredients: The Niche is Now Exposed

As part of the “Playful Crossover” trend, the boba tea market has grown substantially in the U.S., yet many of its core ingredients (tapioca starch, specific packaging materials, specialty teas) are imported from Thailand, Taiwan, and China, all subject to new U.S. tariffs ranging from 10% to over 100%. Even vertically integrated companies like U.S. Boba Co., which produce domestically, rely on imported inputs. Tariff impacts are thus not just felt at the retail end but in upstream manufacturing.

How Kline Can Help

Having worked closely with food companies across sourcing, reformulation, and trends evaluation over the past decade, we understand just how much complexity goes into getting a product from farm to shelf. What’s become clear, especially in the last few years, is that the traditional playbook isn’t holding up anymore. The reality is this: food supply chains were built for stability. For decades, we relied on a global system where efficiency ruled, and costs could be driven down by sourcing from wherever was cheapest. But that model doesn’t reflect the world we’re operating in now. Tariffs come and go with political winds, regulations are tightening across regions, and the assumption that you’ll always be able to ship from point A to point B is no longer safe. Short-term fixes, swapping out a supplier or passing on a price increase might buy time, but they don’t address the root problem. We have to stop reacting to each disruption like it’s an outlier. It’s not. It’s the new baseline. The companies that are positioning themselves for the future are taking a hard look at their value chains and asking, “Where are we vulnerable, and what would it take to not just survive, but thrive, in a system that’s constantly shifting?” That means investment in dual sourcing, in nearshoring where possible, in traceability.

The industry is at a turning point. The food companies that will lead in the next five years will be the ones who took this moment as a signal to build something stronger, smarter, and more flexible.

At a time when volatility is the only constant, navigating ingredient strategy and global sourcing is no longer just a supply chain issue, it’s a boardroom priority. That’s where Kline + Company comes in. With six decades of experience delivering data-driven insights and strategic advisory to the food, beverage, and nutrition industries, Kline helps businesses move beyond reactive decision-making to build resilient, future-proof value chains.

Whether you’re a food and beverage company reassessing ingredient portfolios, exploring reformulation options, or realigning sourcing in response to shifting trade policies, or an ingredient supplier looking to understand how tariffs impact your portfolio, Kline’s industry expertise and market intelligence can guide your next move.

Reach out today to discover how we can help your team turn disruption into strategic advantage.