The move toward lower viscosity, higher VI, lower volatility automotive engine oils demanded by modern vehicles per U.S. ILSAC GF-5 (and, prospectively, GF-6) and European ACEA standards has caused blenders to move to higher-performance Group II+ and Group III, and away from Group I, base oil stocks as they reformulate their recipes. While the initial impacts of these reformulation trends are being felt in the OECD countries, global advancements in engine oil formulations are inexorable.

The move toward lower viscosity, higher VI, lower volatility automotive engine oils demanded by modern vehicles per U.S. ILSAC GF-5 (and, prospectively, GF-6) and European ACEA standards has caused blenders to move to higher-performance Group II+ and Group III, and away from Group I, base oil stocks as they reformulate their recipes. While the initial impacts of these reformulation trends are being felt in the OECD countries, global advancements in engine oil formulations are inexorable.

With demand for engine oil growing sluggishly worldwide, Group I base oils have been squeezed out of automotive lubricants, particularly in North America, by these reformulation trends. Thus, Group I producers are forced to focus more on the industrial sector where they are faced with competition from low-cost naphthenics and Group II oils in many applications. As a result, the proportion of Group I stocks in global base oil consumption has fallen from around 70% in 2000 to 54% in 2012, and it is expected to continue declining to around 30% by 2030.

How does this profound shift in engine oil formulations impact Group I base oil producers? What are the likely pricing consequences for base oils overall and in terms of Group II/III premiums over Group I?

In terms of Group I capacity, the decline in demand has been felt mostly in Europe, which has a disproportionate number of small, independent producers. Within the past year alone, four European Group I plant closures have been announced, while others remain at risk. Western European plants owned by independents are particularly exposed because of their lack of crude price advantage, diseconomies of scale, relatively high labor costs, and lack of backward integration. In addition, certain by-products of Group I base oil production (aromatic extracts and asphalt) are in declining or weak markets, where their refinery conversion values now exceed their traditional arm’s length market prices.

Recognizing the shifts in product formulations required to meet prospective technical standards, many major base oil producers are adding world-scale capacity in the Group II-IV range over the next several years. Chevron’s 25,0000 B/D plant at Pascagoula, MS, plant will by itself expand global Group II capacity by nearly 10% when it comes on-stream later this year.

With overall lubricant demand growth sluggish, projected operating rates on expanding global base oil capacity will remain relatively low in the next five years. This will reduce operating margins throughout the base oil business, contributing to the compression of Group II/III premiums over Group I as the higher-specification materials spill over into traditional Group I markets. Paradoxically, Group I plants are often at the upper end of the manufacturing cost curve, since many lack the scale of more modern Group II/III units and are dependent on by-product (as opposed to mainstream fuel) markets for their non-lube products.

These market forces will continue to drive rationalization of capacity among small-facility Group I producers, notably those in Europe most vulnerable to closure, and put high-cost Group II plants under significant pressure as well. As these high-cost plants shut down, the marginal barrel of Group I will be sourced from larger, more cost-efficient plants whose cash costs are closer to those of higher-VI units. This “New Horizons” scenario will see traditionally Group I-driven base oil price relationships with crude oil and vacuum gas oil move to a somewhat lower pricing threshold more influenced by competition between the surviving Group I plants and their world-class Group II and III competitors.

While this scenario is unfolding before our eyes, the end-game suggests a realignment of fundamental relationships of base oils to crude oil to levels some 5% to 10% lower than historical norms. In addition, the “pricing axis” itself is shifting, driven by the abundant supply of Group II and Group III base stocks. It is no longer sufficient to think in terms of Group I, Group II and Group III pricing, rather we must now think in terms of light viscosity, mid-viscosity, and high viscosity pricing.

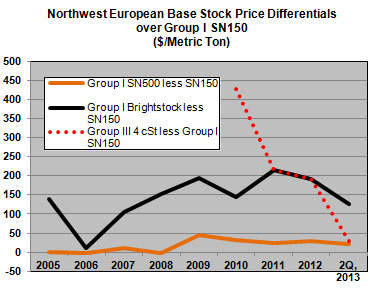

As indicated in the figure, major changes are taking place in terms of inter-Group pricing differentials, with the oversupply of Group II/III capacity worldwide enabling these producers to compete in traditional Group I applications. However, this “spillover” effect is degrading Group III prices, with premiums for VI, NOACK volatility substantially compressed from even recent history. It will be some time before Group III premiums over Group I recover, due to the projected overhang of new capacity construction, and they may never return to pre-2011 levels.

A second impact of the changing landscape for Group I is that demand is dropping fastest in the light solvent neutral grades, which are most impacted by reformulation trends in automotive engine oils. Demand for heavier solvent neutrals and brightstocks is somewhat more robust, which will act to widen the differentials between lower and higher viscosity base stocks over time. In essence, the decline in the value of VI is being replaced by an increase in the value of viscosity.

Though the outlook for Group I is hardly rosy, a core of large, integrated Group I producers will remain, though their focus may change. In Europe, which has to-date not embraced Group II, blends of Group I with Group III and more advanced blend stocks and additives may assure a continuing foothold in the market. In addition, the relatively strong demand for higher viscosity solvent neutrals and brightstocks in industrial and heavy duty applications will provide attractive margins to Group I producers, if they are able to adapt crude selection and process operations to maximize production of the heavier grades and maintain competitiveness on by-product valuation and operating costs. In addition, the strong demand for petroleum waxes, that are only produced in Group I refineries, will help their survivability.