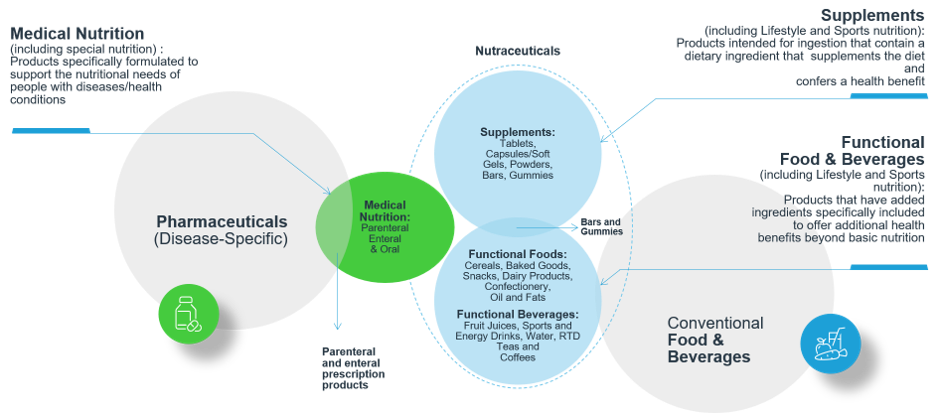

At Kline and Company, we are observing a fundamental shift in how nutrition is defined and delivered. The traditional boundaries between conventional food, dietary supplements, and medical nutrition are increasingly dissolving. What was once a clearly segmented spectrum, with mainstream food on one end and highly regulated medical nutrition on the other, is now evolving into a continuum.

This food and nutrition convergence is giving rise to a rapidly expanding space that sits between these two extremes: specialized and lifestyle nutrition. These emerging categories combine the accessibility and convenience of food with the functional, science-backed benefits traditionally associated with supplements and medical nutrition.

From Segmentation to Spectrum

Historically, the nutrition landscape has been structured in silos:

- Conventional food and beverage focused on taste, convenience, and basic nourishment

- Dietary supplements offering targeted health benefits

- Medical nutrition addressing specific clinical needs under regulatory oversight

However, shifting consumer expectations, driven by preventive health, personalization, and performance, are accelerating food and nutrition convergence, challenging these distinctions, and transforming the market from clearly defined silos into a dynamic continuum. from clearly defined silos into a dynamic continuum.

This shift is most evident in the rapid growth of the functional food and beverage (F&B) category. The market is expected to grow at a CAGR of 7.5–7.8% between 2024 and 2030, nearly doubling to reach approximately $487 billion by 2030, significantly outpacing conventional F&B growth.

Key functional F&B categories and emerging formats include:

- Functional dairy products such as probiotic yogurts, high-protein milk, and dairy alternatives

- Functional beverages including RTD sports drinks, energy drinks, and functional waters targeting immunity, cognition, and gut health

- Protein and active nutrition products positioned for both everyday consumption and performance use

- Bars as a key bridge format, spanning snacks, meal replacements, and targeted nutrition (e.g., protein and fibre bars)

Beyond these categories, there has been rapid expansion into everyday consumption formats, driving the “supplementization” of food across staples, snacks, bakery, and even indulgence categories. As a result, functionality is becoming a baseline expectation rather than a niche feature. At the same time, there is growing demand for more advanced, science-led hybrid formats such as:

- Meal replacements with clinically backed formulations, and

- Performance nutrition products, which increasingly resemble medical nutrition in formulation, if not in regulation

Together, these developments are reinforcing the continued convergence across the spectrum and reshaping the competitive dynamics of the market.

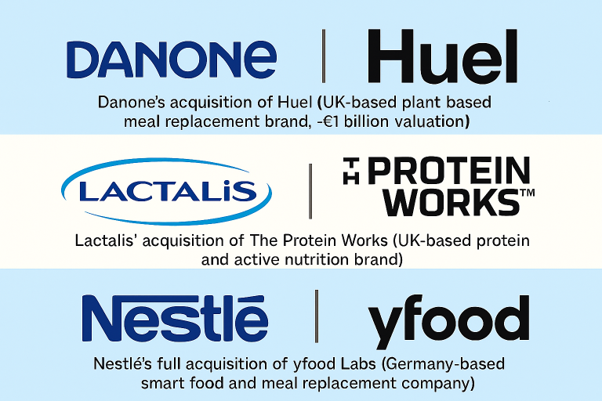

M&A Activity Reflecting the Convergence Trend

The strength and strategic importance of this blurring trend are clearly reflected in some of the most prominent M&A activity of 2026 so far. Major food and dairy players are actively acquiring brands that operate in this “in-between” space, where food meets function and lifestyle meets clinical nutrition.

What These Deals Have in Common

While these companies operate in different niches, the acquisitions share several underlying themes that directly align with the broader blurring of categories:

- Bridging Food and Functional Nutrition

All three brands occupy a space that transcends traditional food categories:

- Huel and yfood offer complete nutrition meal solutions that combine convenience with scientifically balanced formulations

- The Protein Works delivers high-protein, performance-oriented nutrition that appeals to both athletes and mainstream consumers

These are not purely supplements nor traditional foods—they sit firmly in the emerging specialized nutrition segment.

- Targeting Lifestyle-Driven Health Needs

Each brand is built around modern consumer lifestyles:

- Busy, on-the-go consumers seeking convenient, nutritionally complete meals

- Fitness-focused individuals looking for high-performance nutrition

- Health-conscious consumers prioritizing preventive wellness

This reflects a shift away from reactive, clinical nutrition toward proactive, lifestyle-driven consumption.

- Premium, Direct-to-Consumer, and Digital-First Models

These companies have successfully leveraged:

- Strong digital-native brands

- Direct-to-consumer distribution models

- Deep consumer engagement and personalization

This is critical in a category where education, trust, and brand identity are key differentiators.

- Science-Backed but Accessible Positioning

Unlike traditional medical nutrition, which is often prescribed or niche, these brands combine:

- Scientific credibility (nutritional completeness, formulation rigor)

- Mass accessibility (retail, e-commerce, everyday use cases)

This hybrid positioning is central to the rise of lifestyle and specialized nutrition.

- Strategic Expansion by Large Food Players

For Danone, Lactalis, and Nestlé, these acquisitions signal a clear strategic intent:

- Move beyond conventional dairy and packaged food

- Capture higher-growth, higher-margin functional nutrition segments

- Future-proof portfolios against shifting consumer demand

In essence, these companies are repositioning themselves from food manufacturers to nutrition and wellness players.

Conclusion

The acquisitions of Huel, The Protein Works, and yfood Labs are not isolated events, they are emblematic of a deeper structural shift driven by food and nutrition convergence. They illustrate how the leading players are actively investing in the convergence of food, supplements, and medical nutrition.

This blurring is giving rise to a new generation of products and brands that redefine how consumers think about nutrition, not as categories, but as a continuum of solutions tailored to lifestyle and health goals.

Importantly, these acquisitions position companies to tap into high growth, yet still underpenetrated opportunity spaces, including:

- Products designed to support muscle maintenance, gut health, and nutrient absorption in GLP-1 users

- Solutions that address healthy aging, mobility, cognitive health, and metabolic wellbeing in an increasingly aging global population

Growth in this converging space will be underpinned by demand for targeted, high-quality, clinically backed, sustainable ingredient systems such as:

- High-quality proteins (including alternative protein systems) for muscle preservation and satiety

- Biotics (pre-, pro-, post-, and synbiotics) for gut health and broader systemic benefits

- Healthy aging and cellular health ingredients, moving beyond traditional vitamins and minerals

- Cognitive and metabolic support ingredients, including adaptogens, nootropics, and functional fibres

As this space continues to expand, companies that can combine scientific credibility, format innovation, and targeted health benefits, supported by advanced ingredient solutions, will be best positioned to capture the next wave of growth.

What This Means for Ingredient Manufacturers?

For ingredient manufacturers, this convergence represents a significant strategic inflection point. The opportunity is no longer limited to supplying functional components to isolated categories, but rather to enable cross-category innovation through:

- Development of multi-functional, clinically validated ingredient systems

- Greater focus on bioavailability, efficacy, and targeted health outcomes

- Collaboration with brands to co-create format-flexible solutions suitable for beverages, dairy, snacks, meal replacements, and medical-adjacent products

- Alignment with clean-label, sustainability, and personalization demands

The convergence trend is not just expanding demand; it is redefining how value is created in the nutrition ecosystem. Suppliers that can combine scientific depth, functional performance, and application expertise will be best positioned to partner with brands shaping the next generation of nutrition.

As the boundaries between food, supplements, and medical nutrition continue to blur, strategic questions are becoming more complex.

If you’re assessing where to play, how to position, or which capabilities to build, our Food and Nutrition team can help you translate market shifts into clear, actionable strategy.