Yann Pencolé

Vice President, Advisory, Beauty & Wellbeing

The global beauty industry is once again buzzing with speculation. Could Estée Lauder Companies and Puig be heading toward a blockbuster merger?

While both companies have just confirmed they are in talks over a potential business combination, the logic behind such a move is increasingly difficult to ignore. On one side stands Estée Lauder, a $14–15 billion beauty giant navigating a challenging post-pandemic reality. On the other, Puig, a fast-rising €4+ billion fragrance powerhouse benefiting from strong category momentum. The contrast is striking: one restructuring, the other expanding

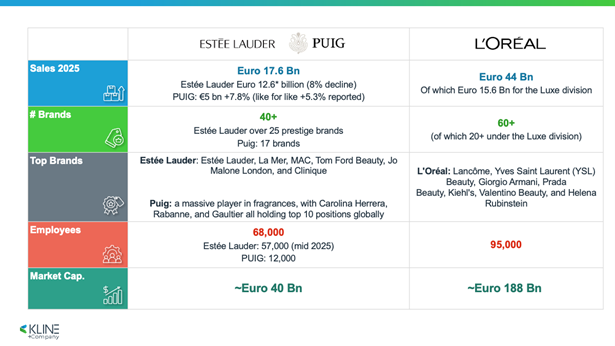

How would Estée Lauder Companies and Puig compare to L’Oréal?

*Reported in USD: $14.3 billion, exchange rate 1.1306 for the period July 2024 to June 2025, fiscal year for Estee Lauder.

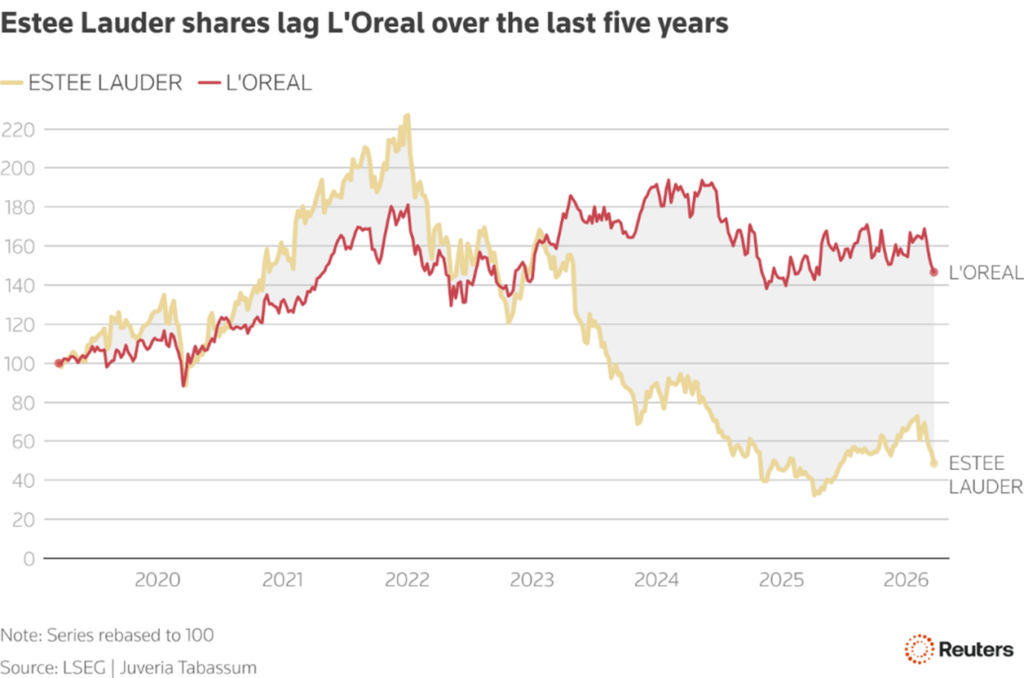

Estée Lauder has faced a sharp slowdown, particularly in Asia. Its share price has dropped over 40% from recent highs, and the company has launched a major restructuring plan, including 3,000+ job cuts to restore profitability. Meanwhile, Puig has surged forward, bolstered by strong fragrance sales and a successful IPO, positioning itself as one of the most dynamic players in the sector.

Kline + Company’s team has been closely following these businesses, and below is our perspective:

The Deal Logic: Why Now? Estée Lauder’s Strategic Reset

For Estée Lauder Companies, this merger would represent more than growth; it would be a course correction.

Estée Lauder reported an annual revenue of $14.3 billion for 2025, marking an over 8% decrease from 2024. These results, ending on June 30, 2025, reflect one of the most challenging periods in the company’s 78-year history.

Fragrance has emerged as the fastest-growing category in beauty, outperforming skin care in key markets. While Estée Lauder owns prestigious names such as Tom Ford Beauty and Jo Malone, Puig brings pure-play fragrance expertise and a proven ability to scale designer scents globally.

Equally important is geography. Estée Lauder’s heavy exposure to China, once a strength, has become a vulnerability not only for fragrance but also for the prestige business, with brands such as La Mer being significantly impacted. Puig offers diversification, with strong roots in Europe and Latin America, helping rebalance global risk.

Add to this the appeal of cost synergies, from shared manufacturing to streamlined distribution, and the merger begins to look like a strategic necessity. For investors, it could signal a long-awaited turnaround and help stabilize a weakened share price.

Source: Reuters

Puig’s Ambition: From Challenger to Giant

For Puig, the equation is different. This is about scale, prestige, and global dominance.

A merger would instantly elevate Puig into the top tier of global beauty, creating a combined entity exceeding $20 billion in revenue. It would gain access to Estée Lauder’s powerful skin care portfolio and deep penetration in North America, two areas where Puig is less dominant.

The portfolios are highly complementary: Puig’s fashion-driven fragrance brands, such as Carolina Herrera and Jean Paul Gaultier, pair naturally with Estée Lauder’s luxury and niche positioning.

Inside the Synergies and Value Creation Potential

As global brand-building becomes increasingly expensive, scale is becoming a critical competitive advantage. At its core, this merger reflects the classic drivers of consolidation:

- Economies of scale in production and sourcing

- Stronger bargaining power with retailers and landlords

- Shared innovation pipelines in fragrance development

- Optimized marketing and distribution

Industry Shockwaves: The Implications for the Competitive Landscape

A deal of this magnitude would ripple across the entire competitive landscape. The impact would be most visible across the following players:

1. L’Oréal: The Leader Under Pressure

The industry’s dominant force would face a newly empowered rival. Already strengthening its position, particularly with the anticipated Gucci fragrance license from Kering, L’Oréal would now contend with a competitor capable of matching its scale in prestige fragrance.

2. LVMH: Luxury Meets Resistance

Home to Dior and Guerlain, LVMH has long dominated high-end perfumery. A merged Puig–Estée Lauder entity could challenge its leadership, particularly in innovation and global reach.

3. Coty: The Squeeze Tightens

After losing its Gucci license, Coty may incur significant losses. Already navigating a complex turnaround, it could face reduced access to licensing deals, increased pricing pressure, and erosion of market share.

4. The Mid-Tier Battle

Interparfums may struggle to secure new brand partnerships, while Shiseido could encounter renewed challenges in repositioning its fragrance portfolio. Amorepacific, although less exposed, is not entirely immune to these shifts.

Asia Rising: The China Factor

Historically dominated by skin care, China is now experiencing a fragrance awakening, driven by younger consumers seeking individuality and self-expression. For Estée Lauder, this is a familiar territory; for Puig, it represents untapped potential.

Together, they could form a formidable force in the region:

- Leveraging Estée Lauder’s distribution strength

- Deploying Puig’s fragrance expertise

- Capturing growth in urban luxury segments

But there is a twist: China is no longer just a market; it is also becoming a creator. Emerging local brands such as Documents, To Summer, Scent Library, and more are beginning to reshape the narrative. While still niche, they hint at a future where China could evolve into a global fragrance innovator.

Outlook: A New Era for Fragrance

If realized, a merger between Estée Lauder Companies and Puig would mark a defining moment for the industry, with several implications:

- Accelerated consolidation among global players

- Intensified rivalry with L’Oréal and LVMH

- Increased pressure on mid-sized competitors such as Coty

- A stronger push into high-growth regions, especially Asia

In the years ahead, the fragrance industry is set to become more concentrated, more competitive, and more global than ever. More importantly, scale, creativity, and strategic boldness will define the winners.

As consolidation accelerates and competitive dynamics continue to shift, beauty leaders will need to reassess where to play and how to win. For those looking to translate these market shifts into clear strategic actions, explore Kline + Company’s Beauty Business Strategy support.