The Latin American (LATAM) region is experiencing a notable upswing in new car sales, driven by economic growth and increasing consumer purchasing power. This surge in demand has created good market conditions for the expansion of Chinese vehicle brands. With competitive pricing, diverse model offerings, and strategic partnerships, Chinese automakers are capitalizing on the growing appetite for new vehicles in Latin America.

However, does this expansion of Chinese OEMs in the region mean business as usual for finished lubricant manufacturers, or is it changing the nature of the game?

Mexico and Brazil are poised to become the hub for regional expansion.

Chinese OEMs’ expansion in the region will have Mexico as the disembarking hub for Central America and the Caribbean region, while operations in Brazil are securing market-entry strategic points for Chinese-branded OEMs in South America.

Initially, Chinese vehicles were mainly available in the market through imports; however, as demand grows, there will be a need to start producing them locally in the region.

According to data reported by AMDA (Mexican Association of Automotive Dealers) based on Mexico’s statistic office INEGI, new car imports from China account for 15% of total imported cars in 2025, which correspond to nearly 250,000 cars. A tremendous leap, considering that in 2020, Chinese vehicle brands held only 4% of the new car sales market.

Due to restrictive trade policies, the focus of Chinese expansion might shift to South America.

As protectionist sentiments regain traction in global trade relations, Chinese OEMs are relocating manufacturing to the region to secure sales associated with tariff restrictions. Mexico and Brazil are the main recipients of Chinese OEM investments.

However, Chinese investments in Mexico have slowed due to trade restrictions imposed by the Mexican government. These restrictions are meant to keep the advantages of nearshoring with the United States.

As a result, Brazil is benefiting as Chinese investments are shifting there instead.

Chinese automakers drive EV adoption in Latin America with affordable and advanced technology.

In terms of technology, the pool of Chinese vehicles is quite diversified, including a mix of internal combustion engine vehicles (ICE), hybrids (HEV), plug-in hybrids (PHEV), and battery electric vehicles (BEV). Chinese automakers such as BYD, Changan, MG, and GWM, and Jetour are some of the top-selling brands in several Latin American countries.

Flexibility, affordable quality, and advanced technology are also fostering electrification in Latin America. Consequently, Chinese EVs are paving the road for boosting EV adoption throughout Latin America.

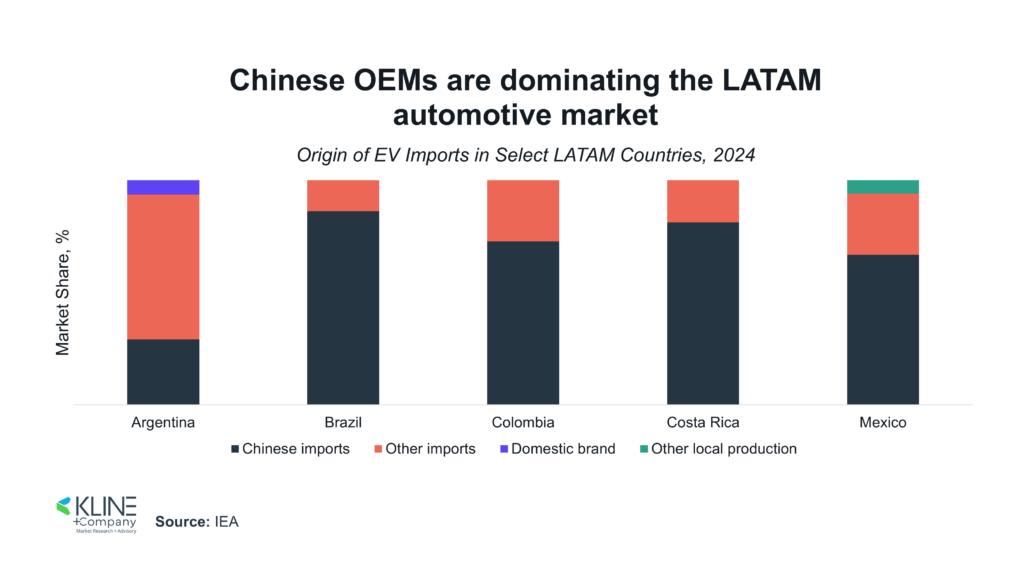

Latin American countries like Brazil, Colombia, and Costa Rica have the highest share of EV imports from China.

One of the main reasons for this success is related to affordability. Chinese electric vehicle models have lower price points compared to the average EVs available in emerging markets, thereby strengthening the competitive advantage of the Chinese automotive industry.

Chinese OEMs are also gaining traction, benefiting from local EV incentives provided in certain countries like Brazil, Chile, and Colombia.

Evaluating the Disruptive Potential of Chinese Vehicle Manufacturers in LATAM’s Lubricant Market

While it is still early to quantify the exact effects on the market volume and value, some preliminary impact scenarios can be assumed, taking into account the specific market dynamics of the LATAM region.

Firstly, we need to consider how effectively Chinese vehicles will influence changes in maintenance practices. Another important factor is the role of lubricant approvals from Chinese OEMs, compared to those from U.S. or European OEMs, which have been established in the region for a long time.

The first notable change in the lubricant market due to Chinese OEM growth will be seen in the factory fill segment. As OEMs based in the region increase their production, the factory fill, and OEM-linked channels in countries like Brazil, Mexico, and others with substantial Chinese vehicle production will be most affected.

In the aftermarket segment, new ICE vehicles and hybrids have the potential to spur demand for lower viscosity grades (SAE 0Ws, and 5Ws).

While upfront prices of Chinese vehicles are competitive, cost of ownership are comparable to legacy vehicles: A potential win for independent workshop (IWS)

Although the sticker price of Chinese EVs is lower than that of the competition, their servicing and maintenance costs are comparable to those of Japanese and US passenger EVs. For this reason, the owners of Chinese EVs are getting serviced in IWS, whose capabilities in servicing electrified powertrains have been growing in recent years. IWS is already preparing for this shift. In Chile, Independent Workshop (IWS) is transitioning toward servicing of electrified powertrains and mechanics are gaining the necessary technical skills for the maintenance of electric vehicles.

How can Chinese vehicle brands influence the importance of OEM approvals in LATAM?

As per Kline’s ongoing research on the LATAM Lubricant market, it suggests that some Chinese OEMs offer less stringent warranty requirements, allowing more flexibility in approvals and recommendations. For example, as long as the engine oil meets the required viscosity grade (such as 0Ws or 5Ws), further OEM spec approval is not necessary. Local companies fill this gap by providing low-viscosity oils (like 0Ws and 5Ws) that might not have OEM spec approval. This trend is seen in Peru, and eventually in other countries in South America.

Several local lubricant suppliers have been quite successful catering this emerging demand pattern, including companies like Vistony in Peru, Bardhal, and Comercial Roshfrans in Mexico.

It is not all about passenger vehicles; Chinese OEMs are also targeting commercial vehicles and motorcycles.

The pace of quality shifts in motorcycle oils (MCO) can also be shaped by new Chinese two-wheeler brands. This is particularly important considering the motorcycle lubricant market is rapidly growing in the region, driven by the expansion of motorcycles, especially personal mobility, and delivery services.

While Japanese OEMs are shifting toward semi-synthetic 10W-30 and 10W-40 engine oils for two-wheelers, Chinese OEMs continue to recommend 20W-50, even for new models.

The LATAM market is not a monolithic market block; there are remarkable differences in terms of regulations and market maturity, among other aspects.

In the commercial vehicle (CV) market, the level of market maturity is a key factor. In Chile, North American and European OEMs in the heavy trucks and machinery sector are predominant, but in Colombia, Peru, and other countries, Chinese OEMs such as JAC Motors, Great Wall, SAIC Maxus, Sinotruck, FAW, are expanding their presence in the trucking segment.

Chinese companies have made substantial investments in countries like Peru, and further expansion is being spurred by investments linked to China in various strategic sectors like mining, construction, ports/logistics (Chancay Port). This, consequently, is driving demand supporting industrial and off-road equipment operations, which are intensive in lubricants (hydraulic, gear oils).

For automotive, lubricant, and aftermarket stakeholders in LATAM, the rise of Chinese OEMs is no longer a future signal but a present‑day inflection point, requiring immediate adjustments in portfolio strategy, OEM engagement, and market execution.